This week, the total rebar inventory nationwide continued to decrease slightly, with social inventory shifting from an increase to a decrease. The total rebar inventory declined by 0.74% WoW, while the total wire rod inventory fell by 2.05% WoW. During the week, construction steel market prices fluctuated downward, with low market trading activity. However, news of production cuts led to a slight rebound, driving speculative demand in the market. Meanwhile, end-use demand continued to recover, resulting in a slight decline in total construction steel inventory this week.

This week, the total rebar inventory stood at 7.9754 million mt, down by 59,800 mt WoW, a decline of 0.74% (previous value: -0.45%). Compared to the same period last year on the lunar calendar, it decreased by 4.074 million mt, a YoY decline of 33.81% (previous value: -35.12%).

Table 1: Overview of Rebar Inventory

Source: SMM

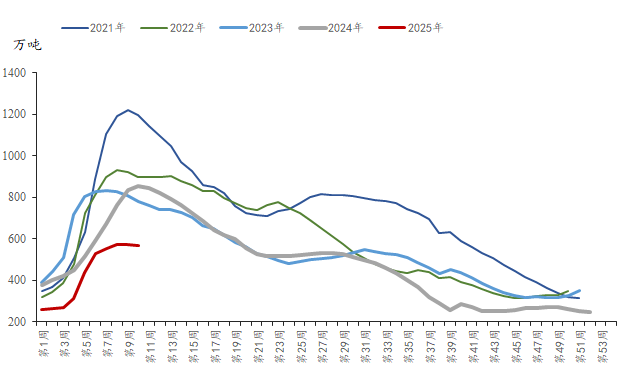

This week, in-plant rebar inventory was 2.2736 million mt, down by 34,600 mt WoW, a decline of 1.5% WoW (previous value: -2.21%). Compared to the same period last year on the lunar calendar, it decreased by 1.5504 million mt, a YoY decline of 40.54% (previous value: -41.18%). Direct supply from steel mills remained relatively stable. However, spot prices weakened during the week, leading to reduced restocking by agents, while production increased slightly. As a result, the decline in in-plant inventory narrowed compared to last week.

Chart-1: Rebar In-Plant Inventory Trends, 2019-2024

Source: SMM

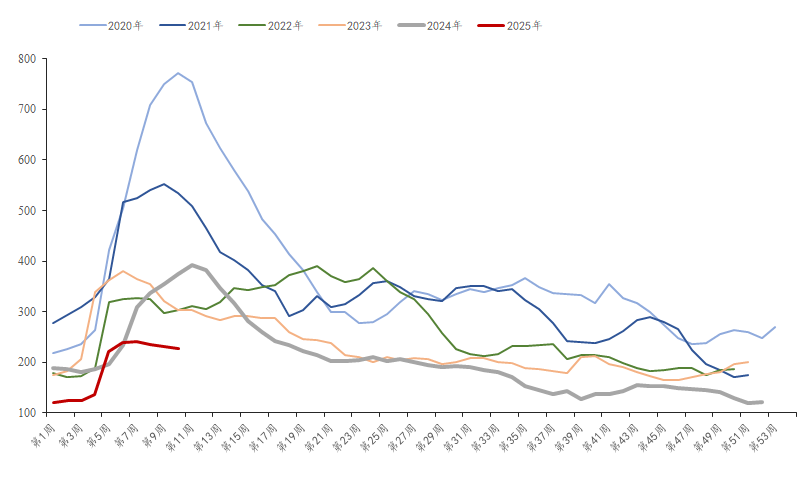

This week, social rebar inventory was 5.7017 million mt, down by 25,200 mt WoW, a decline of 0.44% WoW (previous value: +0.28%). Compared to the same period last year, it decreased by 2.5236 million mt, a YoY decline of 30.68% (previous value: -32.31%). With the accelerated recovery of demand in northern regions, market spot inventory shifted from an increase to a decrease, marking a turning point in social inventory this week.

Chart-2: Rebar Social Inventory Trends, 2019-2024

Source: SMM

Looking ahead, blast furnace steel mills currently maintain certain profitability, and some blast furnaces in north-west China are scheduled to resume production mid-month after maintenance. The capacity utilisation rate of EAF steel mills has recovered to 40.6%, but their operating rate remains constrained by profitability, making further increases difficult. Construction steel production is expected to increase slightly. On the demand side, with the accelerated recovery in northern regions, demand intensity continues to improve. Although the Two Sessions did not bring substantial benefits, coal mine production cuts and steel production controls are boosting market sentiment. Meanwhile, supply growth remains limited. Construction steel inventory is expected to continue destocking next week, with a larger destocking margin.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)